How Do Interest Rates Affect Housing Prices?

“How do interest rates affect housing prices?” is a question I get often with all the news surrounding record low interest rates and the prospect of interest rates rising in the near future. While the interest rate that is mentioned in the news (the Federal Funds Rate) isn’t the interest rate that you would pay for a mortgage, the two are related. With interest rates at a record low, I think it’s time to talk about how different interest rates affect housing prices for the average consumer.

How Are Home Prices Determined Anyways?

Home prices (like any price) are dictated by SUPPLY and DEMAND. The recent surge in prices that we have seen has been caused by multiple factors that affect both of these, but this text below will focus on interest rates, assuming all else is equal (for the sake of explanations).

For home prices the SUPPLY is the number of home sellers in the market (or in a comparable segment of the market, like your local area and price range) and the DEMAND is the number buyers in the market (or in a comparable segment of the market, like your local area and price range). Interest rates affect DEMAND as they impact someone’s ability to buy a home.

How Does Interest Play a Role?

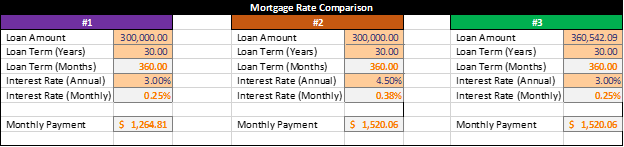

Interest is the cost of borrowing money. If interest rates fall, the monthly cost of a mortgage will fall as well. This also means that when comparing loan amounts, people are able to get a larger loan for the same monthly cost. See the below example:

I’ve listed out the impact of interest rates here on a monthly payment. In #1 and #2 you see the difference in monthly cost of a $300,00 loan based on different interest rates. In #2 and #3 you see the difference in the amount of loan a buyer can have for the SAME monthly payment.

Lowering interest rates makes buying more competitive in 2 ways:

Buyers who want the same house can now afford to pay a higher price for the same monthly payment, meaning they can bid up one another if necessary for a house they want.

Buyers can now afford a bigger house for the same monthly payment they qualified for under the previous (higher) interest rate

For any given property, a lower interest rate will mean there will likely be a combination of MORE BUYERS and BUYERS WHO ARE WILLING TO PAY MORE for any given property (again, all else being equal). This increase in buyers represents an increase in DEMAND, which drives prices up.

The opposite is true if all else is equal and interest rates increase: monthly payments will become less affordable or more money will be needed to keep a smaller monthly payment, and less buyers will be willing to pay for a property as a result.

As you may have guessed, the relationship between interest rates, home prices, and monthly payments tends to drive the market in a way that ends up with the buyer getting a similar monthly payment for a property they are comfortable buying. This is achieved by either paying a higher purchase price when interest rates are lower or paying a relatively lower purchase price when interest rates are higher. Ultimately, it’s up to you to determine what price (and more importantly, monthly payment) are right for your purchase. Now that you’ve learned some basics about the relationships between interest rates and home prices, you can make a more informed decision!